Interest only mortgage loans under scrutiny by ASIC

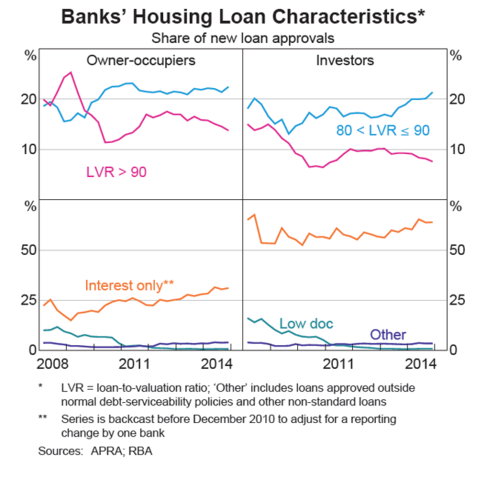

The Australian Securities and Investment Commission (ASIC) are cracking down on interest only loans in the mortgage market suggesting a portion are at risk of default. This is an important initiative on the behalf of the regulator watchdog as in the mortgage market owner-occupiers mortgages interest only repayments equates to over 25% of the market and in the investor mortgage market this statistic is up around 60%. See chart 10.1 below from the March 2015 RBA Financial Stability Review:

Chart 10.1

The ABC News quoted ASIC last week saying:

'Interest-only loans offer a period, typically up to five years, where the borrower only has to pay the interest on the loan, rather than also paying down the principal.

This makes repayments lower in the short-term, but higher over the life of the loan.

'The ASIC review of 140 individual loans found that in more than 30 per cent of cases there was no evidence the lender had considered whether the applicant could afford their repayments over the long term.

ASIC said in 20 per cent of cases the lenders had not considered the actual living expenses of applicants and in 40 per cent of files they had incorrectly calculated the affordability of the loan.' Click here to reference the article.

However, as mentioned in an article from Banking Day yesterday - ASIC's call for better responsible lending compliance easier said than done. ASIC is questioning a large percentage of these loans they have reviewed to date suggesting lending practice regulation were not met. Gadens Lawyers said;

'"ASIC found that most lenders did not appear to be making sufficient inquiries in relation to requirements and objectives or, if they were, lenders were not recording their findings."'

King & Wood Mallesons law firm said;

'"ASIC comments that in the context of an interest-only loan recording the objective or requirement of a borrower is ‘to purchase property’ is insufficient because it does not address why an interest-only loan as opposed to a principal and interest loan would better meet the borrower's objectives... Without ASIC providing guidance on what is appropriate for each type of credit product it is hard to know what will satisfy the obligation."'